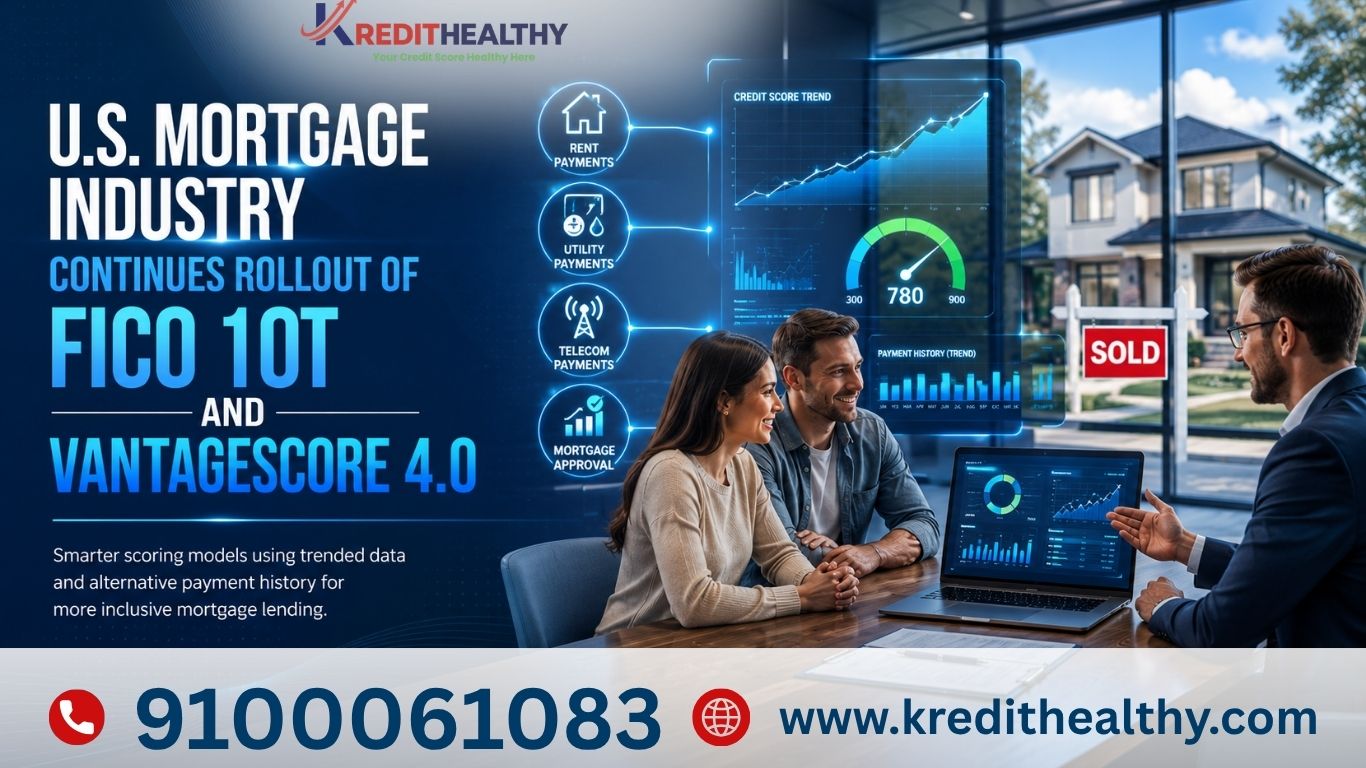

Credit scoring is getting a major makeover this year, affecting how easily millions of people can borrow money for homes, cars, and credit cards.

Lenders are now widely adopting newer models like VantageScore 4.0 and FICO 10T. These updated systems look at “trended data” — your credit behavior over the past two years instead of just a single moment. They also give more weight to alternative payments such as rent, utilities, and phone bills, which can help people with thin credit files.

This shift aims to make credit scoring fairer and more inclusive, especially for young adults, renters, and first-time borrowers. However, many consumers may see their scores move up or down by 20+ points as the new models roll out.

The national average FICO score currently stands at around 715-716, near record highs, while VantageScore averages hover near 701.

Other Key Updates:

More lenders are now including Buy Now, Pay Later (BNPL) payment history.

Paid medical debts and small collections are being removed faster from reports.

Fannie Mae and Freddie Mac are using more flexible scoring for mortgages.

Quick Tips to Protect or Boost Your Score:

Pay every bill on time — it still matters most.

Keep credit card balances below 30% of your limit.

Build positive history by paying rent and utilities on time where accepted.

These changes promise better access to credit for many, but experts advise staying consistent with good financial habits during the transition.